AIA Free Weekly Email 3.12.24

China is winning the energy transition and so is the AIA newsletter

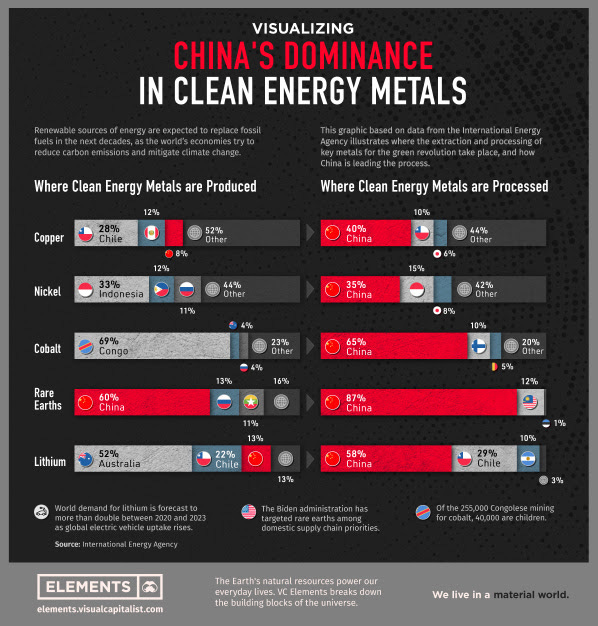

Who is winning the energy transition?

Interesting article from fellow Substacker “Environmental”

The Green Cold War - Part 2

The West’s ill-conceived environmental and energy policies inadvertently gave Russia and China significant geopolitical and economic advantages. This put both countries in a strong position to use energy and other critical commodities as economic weapons to weaken the West.

(skip)

But the West’s attempts to rectify the consequences of almost two decades of interrelated environmental, energy and economic policy mistakes will be politically difficult and expensive. Building more resilient, friendly, and domestic supply chains, especially for the new nuclear power plants that will be key to emissions reduction from electricity generation, will not be accomplished quickly or easily.

(skip)

In addition to China’s near stranglehold on low-cost wind and solar hardware, the West’s obsession with “alternative energy” and “electrify everything” turns out to have given China another critical supply chain advantage: production and processing of critical minerals.

These are the types of situations I look for as a speculator. Governments create policies with no idea how the policy will be carried out in the real world. This creates economic distortions, which we can then profit from by taking the other side of the poorly thought-out policies.

Offshore Oil & Gas E&P Staging A Comeback

The oil industry has found its newest exploration hotspot offshore Namibia. The high success rate of drilling and appraisal activity offshore Africa's southwestern coast is spurring Big Oil to boost acreage in the area and seek other exploration frontiers.

Offshore Namibia, the success rate in discoveries has been phenomenal so far—companies have confirmed 15 discoveries of commercial volumes of oil or gas out of 17 exploration wells drilled since February 2022,

(skip)

Namibia is a key exploration target for supermajors Shell and TotalEnergies, and Portugal-based Galp.

I am very bullish on offshore Nambia, and it is becoming increasingly clear that it is emerging as another prolific offshore basin. I have called it “Guyana 2.0” in the past. I do not think the way to play it is to buy Shell or Total, as any success there will not move the overall needle at those companies. However, in the AIA portfolio, we have a small company with intrests in several blocks offshore Nambia and other areas of the Orange Basin, stretching from Nambia down through South Africa. This company has farmed out some of its interests in these fields to the larger operators with the financial resources and technical expertise to develop these projects. We get a free ride on a carried interest.

THE GREAT PARADOX OF THE U.S. MARKET!

Prices reflect near perfection yet today’s world is particularly imperfect and dangerous

From Jeremy Grantham at GMO

As for the U.S. market in general, there has never been a sustained rally starting from a 34 Shiller P/E. The only bull markets that continued up from levels like this were the last 18 months in Japan until 1989, and the U.S. tech bubble of 1998 and 1999, and we know how those ended. Separately, there has also never been a sustained rally starting from full employment.

The simple rule is you can’t get blood out of a stone. If you double the price of an asset, you halve its future return. The long-run prospects for the broad U.S. stock market here look as poor as almost any other time in history. (Again, a very rare exception was 1998-2000, which was followed by a lost decade and a half for stocks. And on some data, 1929, which was famously followed by the Great Depression.

Regarding the current AI bubble:

But every technological revolution like this – going back from the internet to telephones, railroads, or canals – has been accompanied by early massive hype and a stock market bubble as investors focus on the ultimate possibilities of the technology, pricing most of the very long-term potential immediately into current market prices. And many such revolutions are in the end often as transformative as those early investors could see and sometimes even more so – but only after a substantial period of disappointment during which the initial bubble bursts. Thus, as the most remarkable example of the tech bubble, Amazon led the speculative market, rising 21 times from the beginning of 1998 to its 1999 peak, only to decline by an almost inconceivable 92% from 2000 to 2002, before inheriting half the retail world!

One area of the market that is being overlooked and has not been correlated with the general market over longer periods is energy and metals.

The Actionable Intelligence Alert Newsletter currently holds many energy and metal related companies. Not out of some misplaced nostalgia or because I have a particular affinity for them. It is because they undervalued relative to the market.

If you are interested in learning how I invest using the themes discussed in these free weekly emails, consider a paid subscription to the Actionable Intelligence Alert Newsletter.

Danny at Capital Cosm had me on recently. We discussed the areas I think have opportunity; uranium, gold stocks, emerging markets.

That’s it for this week.

Sell overvaluation, buy undervaluation.

Best regards,

John Polomny

Hope your voice is rested & you’re feeling better, John.

Looking forward to your broadcast Saturday morning 👍