AIA Free Weekly Email 6.25.24

Investment sentiment, liquidity in the system, uranium, precious metals, copper - John Polomny

EPIC RANT: Stop Making THESE Mistakes!:Capital Cosm Interview

I did a couple of recent interviews that you may find interesting. I discuss some things I don’t usually talk about in other interviews. Check out these guys' channels, as they both do some great interviews.

Gold bull market: Why it's still in its early stages - Adam Rozencwajg

Jeremy Szafron, Anchor at Kitco News interviews Adam Rozencwajg, Managing Partner at Goehring & Rozencwajg Associates. In this interview, Rozencwajg provides an in-depth analysis of the current trends in the precious metals market, focusing on gold and silver. With gold prices reaching new record highs and central banks significantly increasing their gold reserves, Adam discusses the implications for investors and the global economy. He also explores the dynamic shift in gold demand from Western to Eastern markets, particularly highlighting the role of China and India. Additionally, Rozencwajg addresses the potential for a short squeeze in the silver market and the impact of de-dollarization efforts by BRICS nations.

The interview is around a month old, but I always like G&R interviews and did not see this one when it came out. My feelings on gold are well known. One should hold a certain amount of physical gold as savings and protection against government and central banks' monetary and fiscal deprivations.

When purchased at the right time, gold stocks can create massive wealth. They are not buy-and-hold investments; they are burning matches and, most of the time, terrible businesses and serial destroyers of capital. However, there are windows of opportunity when they can go on a run. We may be entering a period of time when they will outperform. Stay tuned.

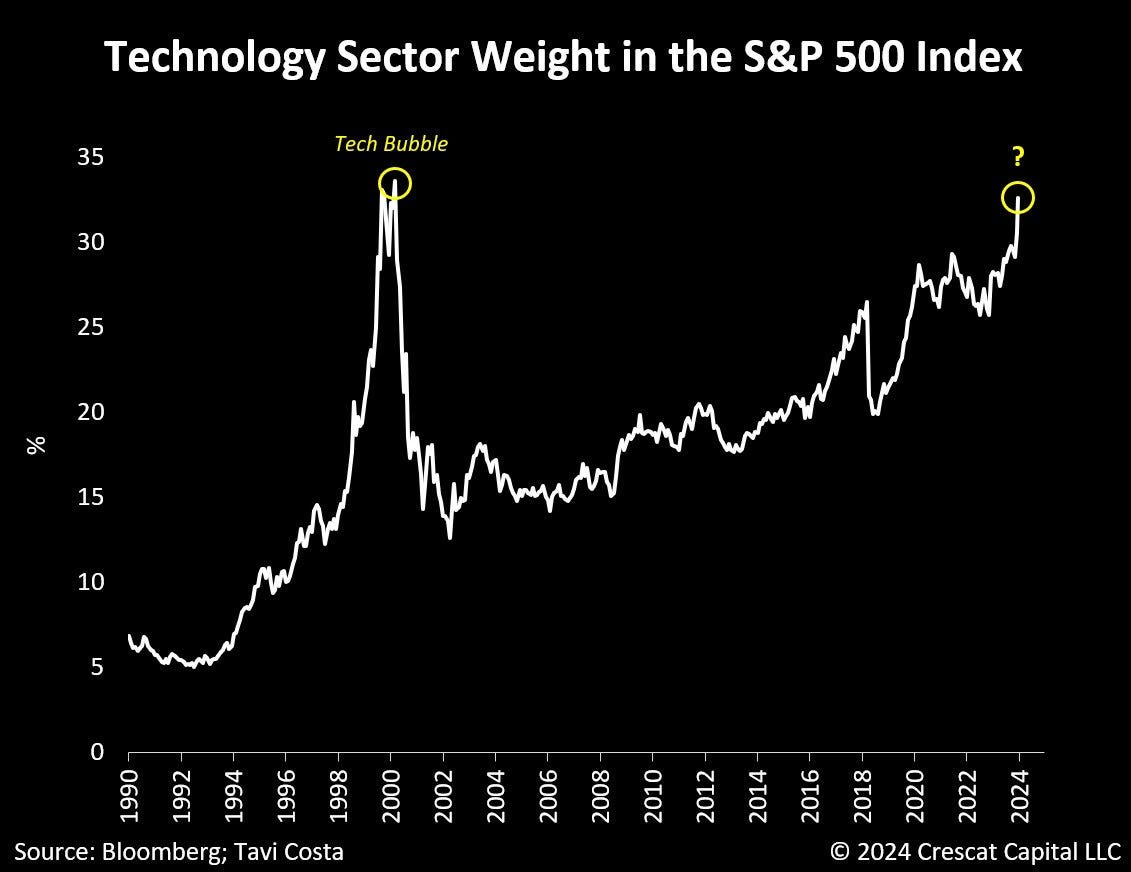

Is Tech On Borrowed Time?

The last time we saw tech at this percentage of the S&P was back during the internet bubble. In the meantime, energy as a percentage of the S&P is still near all-time lows. I like to buy what is out of favor.

Frontier Markets Are Looking Cheap

This is another area of the market in which I am invested (Republic of Georgia, Uzbekistan, etc.). Frontier markets have great potential as they are under-owned, ignored by most investors, and cheap relative to developed markets. Most have decent demographics, and quite a few have low debt as they haven’t had a chance to borrow lots of money.

Many of them are resource-based, and I think commodities and resources will do well over the next decade, so this could be additional wind in these countries’ sails.

I think it will become increasingly important to diversify internationally over the next few years, as I expect the opportunities outside the US to be better than inside the US. Our goal is to consistently compound capital regardless of where we find value.

Maybe The Tech Bros Are Correct

Maybe this time is different, or maybe I have misread the market, and Tech stocks are not overvalued, and they can go even higher. I admit I have no edge in tech stocks, which are way outside my circle of competence.

Buy Nivida selling at 42 times sales? Can’t do it, G!

This has happened before. Sun Microsystems was in the tech bubble back in 2000. The CEO wrote a letter to shareholders explaining why his stock was overvalued.

Sun peaked at a $200bn market cap in 2000, crashed, and was finally sold for $7bn to Oracle a decade later. Their price-to-revenue ratio at the peak was only 10!

They also had decent revolutionary products, from the Java programming language to SPARC processors, StarOffice, MySQL, Solaris OS, VirtualBox, and ZFS! They were involved in all crucial areas of tech.

This is what the CEO wrote to bagholders:

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

Every cycle, we end up with story stocks that rise to outlandish valuations. They all eventually come back to earth. As King Solomon said, there is nothing new under the sun.

That is it for this week.

To your investing success,

John Polomny

This service and my work are reader—and listener-supported. The best way to support me is to follow me on Substack, YouTube, and X. You can also buy me a coffee if you are inclined.

If you want to know how I invest in the themes mentioned in these free emails, please consider a paid subscription to the AIA newsletter.

John, regarding those two recent interviews you shared here: in each one (I think), you mentioned the attractions of a trade in which one would buy some long bonds in anticipation of impending rate cuts and then sell them for some decent capital gain after cuts of appropriate magnitude.

I would love it if you would say a little more about such a trade—what duration bonds would make sense, what catalysts to look for, what attendant risks to consider.

Understood you may not want to go into this. Just wanted to check. Thanks for any thoughts either way.