AIA November 2024

I changed my mind on China

Commentary

I have teased the idea of investing in China on several recent podcasts. As longer-term subscribers will recall, I am a contrarian investor. I look for unloved, unwanted, and hated things in the markets. This usually means they are cheap—in many cases, very cheap. China is currently very cheap.

As Howard Marks says, money is made on an investment when you buy and is determined by what you pay for a particular security. When you buy things that are hated or unloved, you typically get to pay a discount for them. Conversely, when you want to own things everyone loves, you will pay more for that privilege.

Research has shown that the higher the multiple one pays for an investment, the lower the returns.

Meb Faber wrote a paper entitled “Global Value: Building Trading Models with the 10 Year CAPE” that discusses this idea more deeply.

…Valuation is best used as a strategic guide rather than as a short-term timing tool. It is most useful on a time scale of years and decades rather than weeks and months (or even days). While we can formulate a hypothesis for where the S&P 500 ͚should͛ be trading, the animal spirits contained in the marketplace invariably cause prices to deviate quite substantially from ͚reasonable͛ levels, often for years and even decades.

The paper makes the case that using the CAPE ratio (cyclically adjusted price-to-earnings ratio) is an excellent way to determine if a stock or market is over or undervalued. Many will argue, and the paper points out that this is not a great way to measure under or over-valuation. However, it is an excellent way to get to a starting point regarding whether a market is overvalued or undervalued.

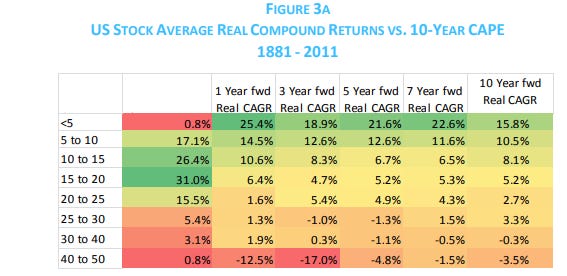

The paper has an excellent chart illustrating my point about returns being tied to the valuation paid.

The data in this paper only goes to 2011, but the point is made: The more you initially pay for a stock, the more likely your forward returns will be lower. The opposite is also true. The less you spend, the more likely your returns will be higher.

From my own investing experience, I have found this to be relatively accurate. This is why I constantly harp about selling overvaluation and buying undervaluation.

This brings us back to China. As I have said for a while, I believe the Chinese market is extremely cheap. The financial media and certain analysts argue that it deserves to be cheap for several reasons. The reasons given are usually the following:

A residential real estate bust has left the country in a massive economic slump and will lead to a banking and/or financial crisis.

It is a communist centrally planned economy.

The US is shifting its emphasis from Europe and the Atlantic to Asia and the Pacific. China is our main competitor in Asia, so a possible military conflict with the US is inevitable.

Out of all of these views, number three influenced me the most. The Russian invasion of Ukraine burned me, and due to sanctions placed on Russia by the US, I incurred a significant loss as I was precluded from selling my securities.

Even though China was and is still cheap, I was hesitant to buy, even though I had added a couple of issues that traded in Hong Kong to my personal portfolio.