Free Weekly Email 1.21.26

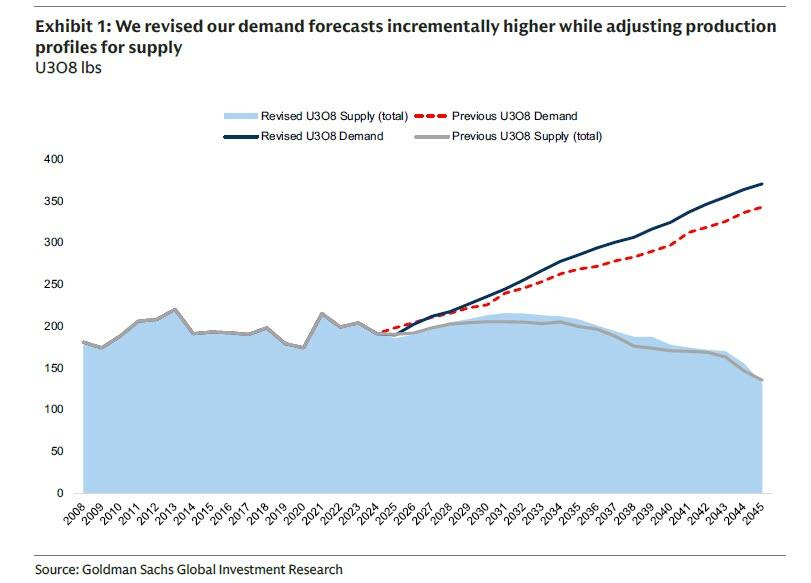

Remember this chart if you are a uranium investor

Lots of demand for uranium, but very little new supply coming online. This is the best supply/demand mismatch in the resource sector.

Time to buy coal?

No need to go crazy with the coal thesis, I just own Glencore for now. Plus, with Glencore, you also get a significant copper producer. They are currently in talks to merge with Rio Tinto, creating the world's largest mining company.

Revenge of the miners

Are you ready?

The great rotation is underway—and it's the one that Robert Friedland has long predicted: the revenge of the miners. For decades, miners were the forgotten sector—underfunded, undervalued, and overshadowed by tech, crypto, and endless financial asset bubbles.

Friedland, the legendary founder of Ivanhoe Mines, called it the "revenge of the miners" years ago: a vindication where the world wakes up to the hard reality that the green/energy transition, electrification, AI data centers, and global growth demand massive new supplies of copper, nickel, gold, silver, and critical minerals—and miners are the only ones who can deliver them.

Robert Friedland makes a compelling case as to why copper is going substantially higher.

Is the IEA Quietly Turning Bullish?

(skip)

During COVID, the IEA’s dire pronouncements helped drive sentiment to extremes—and that despair created one of the best investment opportunities we’ve ever had. Our energy positions purchased during that panic delivered exceptional results. If investors are now reaching for the same pessimism they embraced then, we are more than willing to see how that story plays out a second time.

(skip)

In short, oil prices do not rise when the world runs out of oil. Rather, they rise when investors become so bearish that capital is unavailable, and new production ceases to offset base declines. In 1970, it was the decline of conventional U.S. production. By 2003, the pressure points were the North Sea and Mexico. Today, it is the U.S. shales. These cycles repeat with remarkable regularity, and by our reading, we are simply nearing the end of a long, grinding bear phase.

(skip)

But as we’ve just discussed, the IEA now concedes that demand is likely to keep rising well into mid-century. Under their Current Policies Scenario, consumption climbs toward 120 mm b/d by 2050. To meet that higher level, the industry would need to add roughly 20 mm b/d of new supply—or face a structural deficit. That would require a dramatic increase in investment from today’s levels.

The report also leans far too heavily on future shale contributions. By 2035, the IEA assumes that continued investment will lift shale output from today’s 15 mm b/d to 18 million. Although they do not spell out their assumptions beyond 2035, our reconstruction suggests they effectively assume sufficient ongoing development to keep shale production roughly flat thereafter. Given what we now know about the geology, that is an optimistic reading— one that risks misrepresenting the true durability of shale supply.

The IEA has been consistently wrong about oil supply/demand for many years. They are a globalist organization and are biased to support climate change and the oil demand is peaking agenda. They are likely wrong. if they are then we stand to profit handsomely as the market shifts perception to oil scarcity going forward.

Thats it for this week.

John Polomny

I'm a coal bull since 2021 when I read Ferg's " Coals Moat " bought HCC / SXC , should have bought some others also but now I have GLNCY / AMR / METC/ METCB

I want Yancoal / Thungella / CNR, coal fits my nat gas thesis just like 2021 only this time met coal is in demand

Went heavy in uranium in 2021 also , I believe we are headed for an energy crisis and will need every molecule , I'm installing solar and a wood burner

https://traderferg.com/coals-moat/

Nice information, John. I have noticed that met coal has been slowly grinding higher, up 30% YoY and 13% on the month. Stay warm.