Free Weekly Email 9.18.24

MacroVoices #444 Mike Alkin: Uranium Fundamentals Couldn’t Be Better

Erik Townsend interviews uranium hedge fund manager Mike Alkin. The second half of the interview is the best in my view.

When Smart Money is Wrong

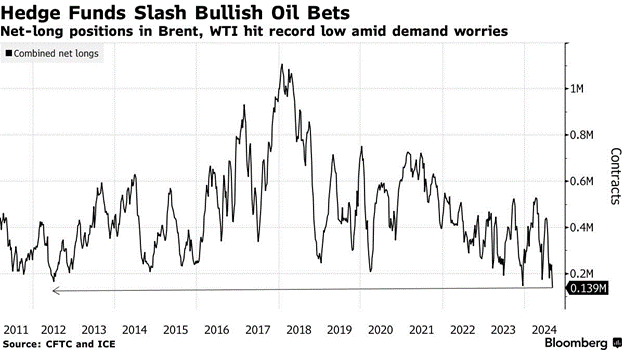

We learned a long time ago that we wanted to know what smart professional investors were doing. It’s always better to know who is smart rather than being smart yourself. Therefore, we’ve constantly kept track of insider buying, what great investors like Warren Buffett and Carlos Slim were doing, and what the most successful hedge funds were up to. A recent chart stopped us in our tracks.

The only time you don’t want to ride along with what the smart money people are doing is when they pretty much all agree. Today, they all agree that oil and gas doesn’t look good for the next six to twelve months.

When everyone is on one side of the canoe I get nervous and I will many times take the opposite side of a trade. It seems everybody is currently bearish on oil and gas (in fact they are record bearish). The price of oil is down as many people think a recession in China and/or the US will cause demand to falter and the price to fall. But is this accurate?

In the worst recession of 2007-2009 since the depression, gasoline consumption dropped 2%. Oil and gas are addictive legal drugs and are scarce resources. Remember, 80% of the U.S. GDP numbers are relatively fixed (think health insurance). The 20% that is variable is what gets whacked in a 3% contraction in the economy.

In the end oil and gas are extractive industries and what is produced needs to replaced. The world has not been doing this. We are also now in a global central bank rate cutting cycle. I expect as these lower intreset rates make their way through the global economy it will begin to accelrate and so will energy demand.

The Future Winners Will Be in Sectors such as Industrials, Materials and Energy

Marko Papic, Chief Strategist at BCA Research, talks about the risk of a bond riot in the US, scenarios for the presidential election, and the most attractive investment opportunities in the coming years.

And just like after 2001, you would say that the US tech sector will not be leading equity markets in the coming years?

Exactly. A leadership change is happening. In the coming years, the winners will be in sectors such as industrials, materials and energy. Everything linked to the big capex topics of rewiring of supply chains and green energy policies. You will want to own indices around the world which have a high percentage of industrials, materials and energy. Europe is an example. Also emerging markets, which everyone is bearish about these days.

Stocks from the commodity complex as well as emerging markets are suffering heavily this year because of the slump in China, though.

We can have a world where China can continue to do poorly, while other emerging markets are doing okay. With regards to commodities: Copper prices are still up 7% year to date, even though China is practically setting itself on fire. This is a good example of where the world is heading. We are in a global capex supercycle not because of China, but because of the other things I mentioned.

And you’d say this supercycle will continue for years?

The collapse of China’s real estate sector is creating a huge headwind, but it’s being overcome by twin tailwinds, which is the rewiring of supply chains and investments into the electrification of the world economy. It’s a step ladder up, and it will continue over the next five years or so.

However, in the short term, the risk of a hard landing of the US economy is adding to the drag for commodities and energy, isn’t it?

Yes. It helps to look at the period of the 1970s for clues. It was a decade which saw a commodity supercycle, but it was interrupted by three recessions, 1974, 1980 and 1981. In recessions, commodities fell every time. If we should have a recession in the next twelve months, I guarantee you that commodities will be down. But what will happen then when the Fed goes all in? I assure you commodities will go up again. So the question is: What is the macro world we live in? Recessions are moments, they don’t change secular themes.

Secular themes don’t change due to recessions. This is what I mean when I say that when one looks back at the end of this decade they will see a chart of tangible assets having gone from the lower left to the upper right. There will likely be observable pullbacks (cyclical downturns within a secular uptrend) in that chart but they will be overwhelmed by the secular forces.

U Need to Focus on Term

I’m writing to you from Zurich, after attending the World Nuclear Association (WNA) meeting a few days ago in London. Last year, the meeting took place in the context of a high $50s (per pound) spot uranium price while this year’s meeting took place with a spot price closer to $80. Normally, a positive return like this would leave investors ebullient, and optimistic for the future. Instead, as I scroll social media, and field questions from friends, I notice a genuine sense of frustration, bordering on fatalism. To me, this seems rather out of place when compared with reality, and the increasingly bullish sentiment from fuel buyers—hence the reason that I’ve chosen to type out this quick missive.

To start with, I find that investors increasingly act like goldfish—fixated on the most recent datapoint, incapable of holding a thought for more than a few seconds. With spot prices having peaked out at over $100 earlier in the year, investors suddenly seem obsessed with the recent soft pullback, while ignoring how we got here. Furthermore, this is all amplified by a general misunderstanding of the uranium market itself.

(skip)

My main takeaway from WNA was that utilities are increasingly hungry, to contract for uranium. Meanwhile, mining companies sense this change in sentiment and have been raising pricing. The data is somewhat anecdotal, but I’ve heard that miners are now quoting $85 floors and $135 ceilings.

I have been telling people for months to ignore the spot market price and focus on the long term contracting price which continues to move higher month after month. I am also focusing on buying the actual commodity (via the Sprott trust) and current or near term producers (companies that are in the process of restarting a previousily closed mine). I find it amusing that I see day after day recently on “X” another “uranium Bro” announcing to Fintiwt that they are throwing in the towel on uranium. They can’t take the volatility, which translates to, “uranium is not doing what I want it to do when I want it to”.

We are in a secular bullmarket in a commodity that is fueling a power source (nuclear energy) that will transform the world. Patience is needed. Recall Buffett’s admonition; “the stock market exists to seperate capital from the impatient and transfer it to the patient”. I believe uranium is a prime example of this advice.

That is it for this week. Thanks for subscribing.

John Polomny

This service and my work are reader—and listener-supported. The best way to support me is to follow me on Substack, YouTube, and X. You can also buy me a coffee if you are inclined.

Good work John.

It will be interesting to see how the stocks market reacts after the Fed Rate decision. I don't think the market has priced in election concerns, the possibility of war, and overvaluation and allocation of tech stocks.