JPOW Prepares The Money Printer

Did the schizo FED just sound game on?

Well, that was an exciting week of FED speak.

Jerome Powell surprised the markets last week when he indicated that the FED was pausing the rate-raising cycle and that cuts in the FED Funds rate may happen sooner than most had anticipated. This ignited risk assets as investors responded to the prospect of lower rates and a potential for a new FED liquidity upcycle.

The Federal Reserve kept rates steady, maintaining the target range of 5.25% to 5.5%, in December, but traders’ attention turned to policymakers’ forecast for rate cuts — including three in 2024. The Fed’s dot plot of central bankers’ rate expectations calls for four more cuts in 2025 and three cuts in 2026.

However, just as fast as Mr. Powell seemed to have popped the champagne cork, several other FED Governors, in particular, New York FED Governor John Williams put the kibosh on the rate-cutting party.

A pair of Federal Reserve officials on Friday threw cold water on Wall Street’s expectations for “imminent” rate cuts.

New York Federal Reserve President John Williams and Atlanta Fed President Raphael Bostic said it’s way too early to consider cutting rates as soon as March – speculation that helped push the Dow Jones Industrial Average to an all-time high this week.

“We aren’t really talking about rate cuts right now,” Williams said in an interview with CNBC, adding that the central bank is still focused on whether it has monetary policy on the right path to continue bringing inflation back to its 2% target.

When I say a schizo FED, here is what I mean.

By the way, The Kobeissi Letter is an excellent account to follow on “X”. Notice that as early as December 1, the FED was saying it was prepared to tighten policy further if necessary. Twelve days later, Powell says rates have peaked, and three rate cuts are coming in 2024. Then, two days later, the NY FED Governor came out and said they “weren’t even talking about rate cuts.” Huh?

See what I mean by schizo. Yet the markets and traders hang on every word these bozo central planners say. Billions, if not trillions of dollars, get committed to buy and sell orders on this nonsense.

So why do we pay attention? Because Mr. Powell and the FED have this huge bazooka of interest rate policy and the ability to print money (which is why they exist, by the way) so it is important to at least know what they are aiming at and when they might fire that bazooka. That bazooka has the potential to massively affect our investments and potential investments.

Yes, if the FED actually cuts rates and/or reinstitutes QE, then risk assets and our investments and speculations will fly. But keep in mind that nothing has actually happened yet, and as was pointed out, they aren’t even talking about rate cuts yet, according to the NY and Atlanta FED governors.

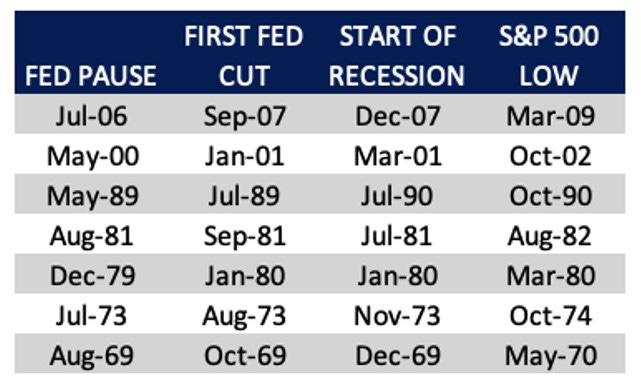

Take a look at the graphic below; it is borrowed from David Rosenberg who is a 40-year-plus veteran Wall Street economist. He is a guy that I like listening to because of his extensive experience and the fact that, as he likes to say, “I still believe in the business cycle”

Notice that history shows that, in many cases, it takes time for rate cuts to positively affect the stock market.

Notice that in previous rate-cutting cycles, the time from when the FED pauses to the first rate cut.

Also, check out the lag effect between the first rate cut and the end of the recession and the low for the S&P 500. Now this is a sampling and does not show every case of recessions and rate cuts. However, there is such a thing as a lag, and it takes time to work through the economy. In fact, when the FED does cut rates, it is very likely we will already be in a recession.

Many people are unaware of this history and how lags work in monetary policy. They try to front-run the FED, which is why you get the volatility we see and are likely to keep seeing.

My base case is that interest rates stay at this level, and the FED continues QT until something breaks in the economy. Then the FED will do what they always do, cut rates very quickly, and depending on the severity of the recession or problem, start QE again.

This will likely lead to a lower dollar, a bull market in emerging markets, and much higher commodity prices and higher prices for the stocks in the AIA portfolio.

We just have to have the patience not to jump the gun and try and get too cute predicting what these people are thinking. Watch what they do, not what they say.

To your investing success,

John Polomny

If you find this analysis useful and are curious about how it applies to specific investing and speculative opportunities consider a paid subscription to the Actionable Intelligence Newsletter.

Really good to see you here on Substack JP.